Global minimum tax and solutions for Vietnam to protect budget, investment attraction

The Global Minimum Tax is approaching and Vietnam needs to take drastic action so the country is not left behind, write country tax leader Thomas McClelland and tax partner Vu Thu Nga of Deloitte Vietnam.

Thomas McClelland, Deloitte Vietnam's country tax leader. Photo courtesy of the company.

Current landscape of global minimum tax

Governments of countries that facilitate outbound and inbound investment activities have been making drastic moves in considering and implementing policies related to the Global Minimum Tax (GMT).

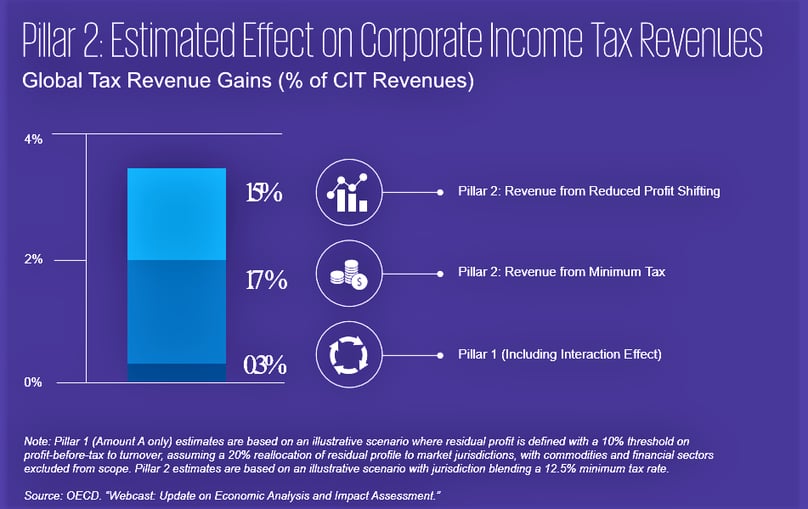

Recently, on December 15, 2022, the EU officially approved a directive to apply a minimum tax rate of 15% from 2024. South Korea has also enacted new GMT rules to align with the OECD BEPS 2.0 Pillar Two after it was passed by its National Assembly on December23, 2022. The regulation will be included in the Adjustment of International Taxes Act and will be effective from 2024. The Japanese government has also announced its Draft Tax Reform, moving towards the application of the GMT from 2024 which will be submitted to the National Assembly for approval.

These countries are large sources of foreign investment in Vietnam and therefore, the official application of the GMT will have several impacts on foreign-invested enterprises. Such impacts will arise soon after the effective time of application in other countries and territories from the fiscal year 2024. Furthermore, Singapore, Malaysia and Hong Kong are heading towards the official application of GMT the same year.

Impacts to Vietnam

The impacts of GMT to Vietnam are clear and urgent in two main areas: taxation and foreign investment attraction.

With respect to taxation, in the event that Vietnam does not take immediate action or delays implementing the GMT, Vietnam may miss the opportunity to have the right to tax, since European countries, Japan, South Korea and others will implement the collection of top-up tax under Pillar Two, most likely starting from 2024. Besides, Vietnam also may not be able to collect top-up tax, if any, from Vietnamese corporations with outbound investment.

In addition, the GMT will also impact foreign investment attraction under the current tax incentives in Vietnam for multinational corporations (MNCs) which are under the scope of the application of Pillar Two. If Vietnam does not take reasonable and timely reforms regarding policy on tax incentives while other countries that are attracting foreign investment have considered measures and favorable investment incentive policies to adapt to the GMT, Vietnam may be left behind.

In such a scenario, not only large MNCs but also satellite enterprises and ancillary enterprises in the value chain could shift their investment from Vietnam to other countries or halt their investment in Vietnam. Malaysia's recent proactive steps in the proposed application of the GMT and Qualified Domestic Minimum Top-up Tax (QDMTT) are initial "warning signals" for Vietnam.

Solutions for Vietnam

Firstly, to protect tax collection, Vietnam can consider an immediate solution of implementing a QDMTT mechanism to gain the right to collect the top-up tax rather than the tax going to another country. QDMTT can simply be understood as a domestic mechanism in which the calculation of excess profits and minimum tax is applied corresponding to the provisions of Pillar Two according to OECD guidelines. This is a measure that some destinations such as Hong Kong, Singapore and Malaysia are considering and are likely to apply.

Despite being considered as a rapid response measure in the context of Pillar Two, the application of QDMTT should be carefully considered taking into account various factors. First and foremost, not all enterprises in Vietnam are subject to Pillar Two, only MNCs with a consolidated annual global revenue of more than EUR750 million ($800.5 million). Accordingly, applying QDMTT to all enterprises would result in negative impacts for enterprises that are not in the scope of Pillar Two but enjoy tax incentives in Vietnam.

In addition, if QDMTT is applied, the calculation of GloBE Income as well as Covered Tax can be complicated and costly, thus it is necessary to weigh the benefits that QDMTT brings in comparison with administrative costs that may have to be spent. On the other hand, Vietnam could apply other domestic minimum tax regimes that are not QDMTT (e.g. direct application of 15% corporate income tax rate in Vietnam without applying the calculation mechanism as of QDMTT).

However, if such a domestic minimum tax regime other than QDMTT is applied, due to the difference in calculation principles, the in-scope enterprises may have to pay additional tax in Vietnam while still having to pay the top-up tax in another country, causing difficulties in tax calculations and declarations.

Secondly, with respect to limiting adverse effects on attracting foreign investment, Vietnam should introduce cost-based incentive mechanisms and policies to support businesses that are enjoying tax incentives and affected by Pillar Two. Currently, the Vietnamese regulations on corporate income tax incentives are not manifold, focusing mainly on income-based incentives such as tax incentives and tax exemptions. Cost-based incentives, especially cash grants, are still limited.

Income-based incentives are relatively common in developing countries, while developed countries tend to rely more heavily on cost-based tax incentives such as accelerated depreciation, investment subsidies or tax credits rather than broad-based income tax holidays, according to an OECD report. The advantage of incentives based on income is easy to manage since they are usually declared at the year-end tax finalization, while at the same time there is no upfront payment from the state budget. It is also attractive for new investment projects that could quickly generate profits in the early stages. However, the disadvantage of income-based incentives is that there may be cases of transfer pricing to shift profits to countries with large profit-based incentives.

Furthermore, although income-based incentives can attract new investment projects and large profits in the early stages, they may not be attractive for expansion projects since the incentive policy for expansion projects may be lower than for new investment projects. In addition, income-based incentives are generally applied for a certain period of time (for instance in Vietnam, tax exemption can be applied within two years or four years, tax reductions can be granted for four years or nine years).

Therefore, there are cases where businesses liquidate when the incentive period expires in order to apply for a new investment project or shift the investment to other countries to enjoy new incentives. As a result, income-based incentives in the long term will have certain limitations, especially in the context of the application Pillar Two being, the benefits of income-based incentives will be significantly reduced for in-scope enterprises.

Compared with income-based incentives, cost-based incentives such as cash grants to partially cover the cost of investments in fixed assets, R&D activities or human resources, have the advantage of being able to encourage substance and long-term investment activities (such as large investments in facilities, machinery and factories, investment in R&D activities, etc.), including expansion of investment activities at a later stage, and limiting profit shifting or short-term investments. Although cost-based incentives may result in an upfront payment from the State budget, such payments are however easy to estimate based on the value of the investment and independent from the business results, therefore it is appropriate for budgeting purposes.

It is noteworthy that the application of cash grants is also being considered by countries, such as Malaysia, in continuing to attract and retain foreign investors, thus it may adversely affect the investment attraction environment of Vietnam in case such a scheme is approved for implementation. Besides, some expenditure-based incentives aiming at incentive diversification and encouragement of substance investment activities, such as super expense deduction for R&D activities, intellectual property registration, etc. are relatively common in other countries, such as China, Singapore and Malaysia.

Having said the above, cash grants should be carefully considered because of the potential impact on the state budget, the increased administrative procedures, as well as subject to a comprehensive study in reference to the OECD guidance on Pillar Two, for example, whether the issuance of cash grants will affect the application of QDMTT (in case Vietnam chooses this option), and how it specifically impacts the calculation of effective tax rate (ETR) of the enterprise following the OECD formula.

Other recommendations

The GMT is approaching and Vietnam needs to consider and take drastic action so the country is not left behind. Deloitte Vietnam would like to set out some recommendations as follows and will continue to discuss and accompany competent authorities in the process of developing fair and reasonable policy solutions to help protect tax revenue while continuing to attract investment in Vietnam.

Firstly, Vietnam needs to prepare in all aspects from now for the official application of Pillar Two, in the context that many countries will apply the GMT in 2024. Policies to cope with the impacts of Pillar Two should be developed in the short term as well as the long term.

In the short term, early consideration should be given to the application of the domestic minimum tax mechanism that meets the standards of QDMTT to gain the right to collect taxes which is in line with OECD rules taking into account the benefits and costs if implemented.

In the long run, the taxation system along with incentives should also be considered for reform in order to limit the negative impacts of Pillar Two to ensure the attraction of substantial investment, and to limit activities that erode the tax base and profit shift.

We would like to note that the issuance of any new policy or mechanism requires a comprehensive study and careful analysis to ensure fairness amongst businesses that are both in and out of the scope of Pillar Two and to ensure consistency with the regulations on ensuring investors' interests under the current Law on Investment, as well as not violating international commitments and OECD rules to which Vietnam is a member. We understand that shortly the Ministry of Finance and the General Department of Taxation will also make impact assessments to prepare for the appropriate policy changes to come.

Secondly, to support the MNCs which are affected by Pillar Two, new forms of cost-based investment incentives, especially cash grants, should be weighed against other incentives taking into account the pros and cons in comparison to income-based incentives. Vietnam should consider reforming its tax incentives system to be more appropriate in the new situation by referencing and consulting with the OECD, as well as the policies being implemented by other countries.

Lastly, the Vietnamese government should strengthen the personnel of the Prime Minister's Task Force Team on the GMT as soon as possible and should quickly develop a domestic legal framework related to the application of the GMT to ensure that incentive policies for foreign investors in Vietnam are efficiently implemented.

The Investor (www.theinvestor.vn) will hold a workshop on Friday to discuss solutions to maintain and improve Vietnam’s competitiveness and lure FDI as countries across the world prepare to implement the global minimum tax (GMT).

Participants will include representatives of the Ministry of Finance, Ministry of Planning and Investment, business associations, Vietnamese and foreign investors, economic experts, and "Big 4" auditing companies.

Time: 8:30 am, Friday, February 24, 2023

Venue: Floor 1, Ministry of Planning and Investment office building at 65 Van Mieu street, Hanoi.

- Related News

- Read More

Half of Swedish businesses operating in Vietnam plan investment expansion

The fact that 50% of surveyed Swedish businesses plan to increase investment in Vietnam in 2026 demonstrates their firm long-term confidence in the Vietnamese market.

Industries - Thu, June 18, 2026 | 1:53 pm GMT+7

Vietnam seeks deeper nuclear cooperation with Russia's Rosatom

Vietnamese Prime Minister Le Minh Hung called for expanded cooperation in nuclear energy with Russia's Rosatom, including support for Vietnam's planned Ninh Thuan 1 nuclear power plant, at a meeting with CEO Alexey Likhachev on Wednesday.

Energy - Thu, June 18, 2026 | 1:38 pm GMT+7

Vietnam PM backs expanded energy cooperation with Russia's Zarubezhneft

Vietnamese Prime Minister Le Minh Hung met with Sergei Kudryashov, CEO of Russian state oil company Zarubezhneft, on Wednesday and expressed support for expanding bilateral cooperation in oil and gas, offshore wind power and other energy projects.

Energy - Thu, June 18, 2026 | 12:26 pm GMT+7

Vietnam central bank proposes easing limit on short-term funds for long-term lending

The State Bank of Vietnam has proposed raising the maximum ratio of short-term funding that commercial banks can use for medium- and long-term lending from 30% to 40%, marking a reversal of years of tightening aimed at reducing maturity mismatch risks.

Banking - Thu, June 18, 2026 | 11:16 am GMT+7

EVNGENCO3 completes over 50% of year's profit target, accelerates investment in new power projects

Vietnam's Power Generation Corporation 3 (EVNGENCO3) has completed nearly 55% of its full-year profit target after the first five months of 2026, supported by resilient electricity demand and stable system operations, while stepping up investments in LNG-fired power, battery energy storage systems (BESS) and renewable energy projects.

Investing - Thu, June 18, 2026 | 8:17 am GMT+7

Vietnam Rubber Group plans capital hikes for listed subsidiaries as earnings climb

Vietnam Rubber Group (HoSE: GVR) plans to raise capital at several of its listed subsidiaries, starting with Phuoc Hoa Rubber, as the state-controlled giant seeks to strengthen its subsidiaries while benefiting from high rubber prices and expanding industrial park operations.

Companies - Wed, June 17, 2026 | 8:14 pm GMT+7

Vinhomes to cease land bank expansion in Vietnam, focus on capitalizing on existing projects

Vietnam’s largest listed property developer Vinhomes, a subsidiary of Vingroup (HoSE: VIC), will stop acquiring new land in the domestic market, shifting its focus toward developing its existing portfolio and extracting greater value from projects already under its control, chairman Pham Thieu Hoa said.

Companies - Wed, June 17, 2026 | 5:19 pm GMT+7

State-controlled machinery firm VEAM announces highest dividend payout in 4 years, stock listing still on hold

Vietnam Engine and Agricultural Machinery Corporation (VEAM) plans to pay more than VND6.96 trillion ($264.46 million) in dividends for 2025 at a payout ratio of 52.4%, its record high in four years, while its long-delayed stock exchange listing remains on hold due to unresolved legacy issues.

Companies - Wed, June 17, 2026 | 3:30 pm GMT+7

Aeon Mall Vietnam achieves double-digit growth in 2025, accelerates network expansion

Japan’s retail giant Aeon Mall continued to record strong growth in Vietnam last year while accelerating the expansion of its network in Danang, Thanh Hoa, Quang Ninh, and several other localities across the country.

Economy - Wed, June 17, 2026 | 2:53 pm GMT+7

Palm City project enters new development phase as Palm River subdivision launched

Nam Rach Chiec Company Limited, together with Huong Viet Properties, recently held the Palm City Urban Area kick-off ceremony and officially launched the Palm River subdivision, marking the beginning of a new development phase for the 30.2-hectare urban township in Ho Chi Minh City.

Real Estate - Wed, June 17, 2026 | 11:27 am GMT+7

Petrovietnam's assets top $44.8 bln in 2025, profit jumps 39%

Petrovietnam ended 2025 with total assets exceeding VND1,178 trillion ($44.8 billion), up nearly VND100 trillion ($3.8 billion) from a year earlier, while reporting a 39% increase in net profit and maintaining one of the country's largest cash positions.

Companies - Wed, June 17, 2026 | 8:00 am GMT+7

Coteccons dismisses concerns over executive departure, competition from Vingroup's arm

Vietnam's leading contractor Coteccons (HoSE: CTD) said a recent change in senior management was unrelated to the company's share price performance, as executives highlighted record order backlog and accelerating earnings growth amid a recovery in Vietnam's construction industry.

Companies - Tue, June 16, 2026 | 5:26 pm GMT+7

VinaCapital lists 2 strategic ETFs as Vietnam fund market broadens

Vietnam’s leading investment management firm VinaCapital has listed two strategic exchange-traded funds (ETFs) on the Ho Chi Minh City Stock Exchange, expanding investment options for investors seeking targeted exposure to Vietnam's long-term economic growth themes.

Finance - Tue, June 16, 2026 | 4:39 pm GMT+7

Oil & gas industry gives Vietnam edge in offshore wind supply chain: Global Wind Energy Council CEO

Vietnam is well positioned to play a significant role in the offshore wind power supply chain thanks to its established manufacturing base and expertise developed through its oil & gas industry and existing wind power projects, according to Ben Backwell, CEO of the Global Wind Energy Council (GWEC).

Energy - Tue, June 16, 2026 | 4:31 pm GMT+7

Vietnam banking, retail, oil stocks well placed for market recovery: brokerages

Vietnamese banking, retail and oil-gas stocks are among the sectors best positioned to benefit from a potential market recovery after months of pressure from geopolitical tensions and macroeconomic headwinds, according to local brokerages.

Finance - Tue, June 16, 2026 | 1:04 pm GMT+7

Petrovietnam, Huawei discuss cooperation in digital transformation, AI, energy technologies

State-owned Petrovietnam and China's Huawei Technologies discussed potential cooperation in digital transformation, artificial intelligence and digital energy infrastructure during a meeting last week, as the Vietnamese giant seeks to modernize its operations and expand into new energy sectors.

Companies - Tue, June 16, 2026 | 12:20 pm GMT+7