Apartment prices in Hanoi rise for 20 consecutive quarters, ease in HCMC

The average primary prices of apartments in Hanoi have increased for 20 consecutive quarters amid scant supply while those in Ho Chi Minh City have cooled down, according to the latest Savills Vietnam report.

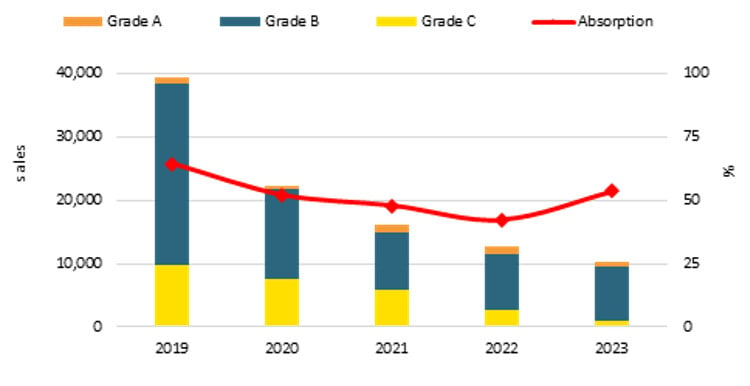

Primary asking prices of VND58 million ($2,363)/m2 net sellable area (NSA) in the fourth quarter of last year increased 7% quarter-on-quarter and 12% year-on-year.

The primary apartment stock of 11,911 apartments in Hanoi dropped 40% quarter-on-quarter and 41% year-on-year.

Hanoi apartment performance. Source: Savills Vietnam.

There is a disconnect between demand and supply in Hanoi, especially for affordable properties, explained Do Thu Hang, senior director of advisory services at Savills Hanoi, adding metro lines and ring roads will accelerate decentralization when completed.

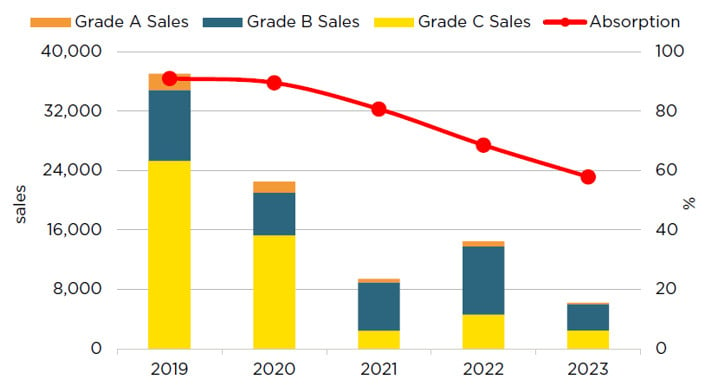

In contrast, primary apartment prices in Ho Chi Minh City in Q4/2023 returned to the 2020 level at VND69 million ($2,810)/m2 NSA, down 36% quarter-on-quarter and 45% year-on-year.

Primary stock in the city has trended downwards since 2017. In Q4/2023, primary stock of 7,600 units was stable quarter-on-quarter but dropped 5% year-on-year.

Ho Chi Minh City apartment performance. Source: Savills Vietnam.

Residential stock in HCMC is in incredibly short supply, especially considering that the city’s population exceeds 10 million, Giang Huynh, head of research and S22M noted.

According to Savills Q4/2024 apartment market report, in HCMC, apartment returns have softened for five years, however, they remain above deposit interest rates. As such, apartments continue to be a profitable investment channel, said Giang.

A similar tendency has been observed in the residential market by CBRE Vietnam, another foreign-invested real estate services firm.

In 2023, both Hanoi and HCMC experienced the lowest number of new apartments in the past 10 years. In Hanoi, nearly 10,300 condominiums and 2,600 landed property units were launched last year, down 32% and 84% year-on-year, respectively.

In HCMC, there was a more modest new supply with nearly 8,700 condominiums and only 30 new landed property units launched, representing a decline of 54% and 98%, respectively, compared to 2022.

However, there was an improvement in the number of newly launched units in the latter half of 2023 compared to the first half, particularly a significant increase of over 60% in the Hanoi condominium market and an 11% increase in HCMC.

Mega-urban projects in the west and east of Hanoi and in the east of HCMC continued to dominate the market with the highest share of new supply in both cities, contributing more than 60% of new supply in Hanoi and nearly 80% in HCMC.

Primary selling prices of condos in both cities remained high, especially in Hanoi, with primary prices recording a rapid price growth mainly due to the large quantity of new supply in the high-end segment. The number of high-end condominium units accounted for 75% in Hanoi and 84% in HCMC of 2023’s total new launches.

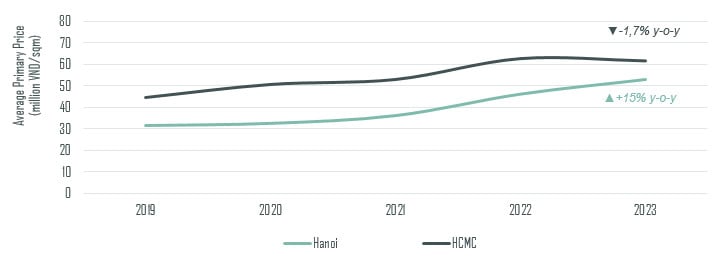

Average primary prices in Hanoi and HCMC in $/sqm (excluding VAT and maintenance fees, quoted on NSA). Source: CBRE Research, Q4/2023.

On the other hand, the mid-end segment, with selling prices more budget-friendly to the majority of the population, accounted for only a small proportion, while the affordable segment has completely disappeared in both markets in the past few years.

“In 2023, we observed a reversal in the trend between the Hanoi and HCMC residential markets, with the Hanoi market now following a similar trajectory to that of HCMC about three years ago," said Dung Duong, executive director of CBRE Vietnam. Particularly, at the end of 2023, the average primary selling price in Hanoi reached VND53 million ($2,159)/sqm (excluding VAT and maintenance fees), up 4.6% quarter-on-quarter and 14.6% year-on-year. This was the primary price recorded in HCMC during the 2020-2021 period.

On the contrary, primary prices for condos in HCMC levelled off at around VND61 million ($2,485)/sqm in 2023, down 1.7% year-on-year. During 2023, high-end supply located far from the city center and mid-end supply were higher than the previous year.

In the secondary market, selling prices of condos in Hanoi and HCMC went on opposite trends. Secondary prices in Hanoi in Q4/2023 continued to increase from the previous quarter, reaching around VND33 million/sqm, up 5% year-on-year. Limited new supply an newly launched projects setting high prices contributed to boosting the demand in the secondary condominium market in Hanoi.

In contrast, secondary prices in HCMC recorded VND45 million/sqm for the condominium market and VND140 million/sqm for the landed property market on average, down 5% and 2% year-on-year, respectively. During 2023, the secondary market in HCMC went through several price adjustments, yet the price fall gradually slowed towards the last quarter.

Landed property in Hanoi experienced the same trend, with a gradual decrease in the number of distressed sales in the secondary market since the second half of the year, resulting in a slowdown in price declines towards the end of the year. In Q4/2023, the average secondary price of landed property in Hanoi reached nearly VND157 million/sqm, down 5% year-on-year.

A corner of Hanoi. Photo courtesy of VietNamNet.

In terms of absorption rate, Hanoi and HCMC recorded more than 22,000 residential units sold (including both condos and landed properties) in 2023, representing only half of the units sold in 2022.

However, there was an improvement in the absorption rate in the second half of 2023, thanks to the proactive efforts of developers. These efforts included implementing preferential sales policies such as extended payment schedules and discounts of up to 40% for early payment.

Additionally, positive macro factors such as declining interest rates have contributed to improved sentiment among home buyers. As a result, the number of residential units sold in the last two quarters of the year helped to increase the sold units by more than 60% in Hanoi and they doubled in HCMC compared to the first half of the year.

CBRE Vietnam expects an increase in new supply in both cities in 2024. In Hanoi, the market is expected to welcome nearly 16,000 condos and more than 6,000 landed property units, mostly from mega-urban projects in the west and east.

Meanwhile, HCMC expects new supply of over 9,000 condos and 1,000 landed properties in 2024. In the short term, new supply is still limited, while demand remains high, causing selling prices to maintain a high level.

“The policy interest rate is on the stabilizing track, and there are upcoming approvals and amendments to policy and legal frameworks that will contribute to increased synchronization and consistency for the real estate environment. These factors will increase buyer sentiment and facilitate market recovery in 2024,” commented Dung Duong from CBRE.

- Read More

Masan High-Tech Materials partners with S Korea’s GBI on tungsten processing

Masan High-Tech Materials (UPCoM: MSR), the mining unit of Vietnamese conglomerate Masan Group (HoSE: MSN), has entered into a strategic partnership with South Korea’s GB Innovation (GBI) to process Korean tungsten concentrate into higher-value products in Vietnam, strengthening a non-Chinese tungsten supply chain.

Companies - Thu, July 9, 2026 | 3:51 pm GMT+7

Idemitsu Kosan expands energy ecosystem in Vietnam

After more than three decades of operations in Vietnam, Japan’s Idemitsu Kosan is further expanding its energy ecosystem with a biomass pellet plant project in the central province of Gia Lai.

Industries - Thu, July 9, 2026 | 1:43 pm GMT+7

Two banks to list on Ho Chi Minh City bourse, expand charter capital

Vietnam's private banks Vietbank and BVBank are finalizing the last steps to transfer their trading from the unlisted public company market UPCoM to the Ho Chi Minh Stock Exchange (HoSE), while simultaneously implementing plans to increase their charter capital.

Banking - Thu, July 9, 2026 | 11:51 am GMT+7

Strong Q2 earnings, lower interest rates to bolster Vietnam stocks

Strong second-quarter corporate earnings and declining interest rates are expected to support Vietnam's stock market in the coming months, brokerage firms said, as the market moves beyond a period of limited news flow and enters a more favorable phase driven by improving fundamentals.

Finance - Thu, July 9, 2026 | 8:00 am GMT+7

Wistron raises construction, equipment investment in northern Vietnam province to $178 mln

Taiwanese technology firm Wistron has increased its investment in factory construction and equipment in Ninh Binh province to $178.27 million, adding $24.5 million to expand its facilities at Kim Bang Industrial Park.

Industries - Wed, July 8, 2026 | 7:56 pm GMT+7

Sun Group targets groundbreaking for $624 mln urban projects in central Vietnam this year

Vietnam's leading developer Sun Group aims to begin construction of two urban projects worth a combined VND16.4 trillion ($623.78 million) in the central province of Quang Ngai by the end of 2026, while also advancing plans for a new expressway linking the province with the Central Highlands.

Real Estate - Wed, July 8, 2026 | 4:54 pm GMT+7

Vietnam raises airport number target to 36 by 2030 as aviation demand surges

Vietnam plans to expand its airport network to 36 airports by 2030, up from the previous target of 30, under a revised national aviation infrastructure plan aimed at catering for rising passenger demand and boosting regional connectivity.

Infrastructure - Wed, July 8, 2026 | 4:45 pm GMT+7

Germany's VFT Bio Fuels UG eyes $3.1 bln green steel complex in southern Vietnam

Vietnamese industrial park developer IMG Phuoc Dong and Germany’s VFT Bio Fuels UG have signed a memorandum of understanding to study the development of a $3.1 billion green steel complex in the southern province of Tay Ninh.

Industries - Wed, July 8, 2026 | 4:25 pm GMT+7

Vietnam police minister urges Yamato Holdings to study investment in Gia Binh airport

Vietnam’s Minister of Public Security Luong Tam Quang has called on Japan’s Yamato Holdings to assess investment opportunities in warehousing and cargo transport systems at Gia Binh International Airport, while exploring potential cooperation and operational models with Vietnamese partners once the facility becomes operational.

Infrastructure - Wed, July 8, 2026 | 3:09 pm GMT+7

Vietnam real estate M&A favors quality, clear legal status assets as FDI priorities evolve

Vietnam's real estate M&A market continued to attract foreign capital in the first half of 2026 despite persistent global economic uncertainties, but foreign investors are increasingly targeting assets with clear legal status, stable cash flow, and strong operational performance, with data centers emerging as a key growth segment.

Real Estate - Wed, July 8, 2026 | 1:38 pm GMT+7

Central Vietnam hub Danang plans to tokenize nearly $4 bln in infrastructure projects to attract global capital

The Vietnam International Financial Center, located in the central city of Danang (VIFC Danang), plans to tokenize nearly $4 billion worth of infrastructure projects as part of a strategy to attract more global capital.

Economy - Wed, July 8, 2026 | 12:17 pm GMT+7

Computers, smartphones edge higher in price as AI memory boom tests Vietnam's ICT firms

Rising memory chip prices driven by artificial intelligence are spreading from semiconductor manufacturers to consumer electronics brands such as Apple, Dell and ASUS, pushing up the prices of computers and smartphones.

Companies - Wed, July 8, 2026 | 8:00 am GMT+7

LG Innotek to build $1 bln semiconductor substrate plant in northern Vietnam

South Korea's LG Innotek will spend $1 billion to build a semiconductor package substrate manufacturing plant in Hai Phong city, with mass production scheduled to begin in the third quarter of 2028, according to local authorities.

Industries - Tue, July 7, 2026 | 11:13 pm GMT+7

Malaysia’s JLand eyes up to $6 bln high-tech hub in Hanoi

Malaysia’s JLand Group has proposed developing a high-tech, innovation and data center complex in Hanoi with an estimated investment of $4-6 billion, as Vietnam’s capital seeks to attract technology projects and strengthen its digital infrastructure.

Infrastructure - Tue, July 7, 2026 | 4:26 pm GMT+7

PVOIL approves $600 mln crude supply plan for Nghi Son refinery

PVOIL, a subsidiary of state-owned Petrovietnam, has approved transactions worth an estimated $600 million to supply crude oil to the Nghi Son Refinery and Petrochemical complex during the second half of 2026, as the country’s largest refinery broadens its feedstock sources beyond its traditional Kuwaiti supply.

Companies - Tue, July 7, 2026 | 1:33 pm GMT+7

F88 wins two international awards for customer-centric growth strategy

F88, a major Vietnamese financial services company, has received two international awards from the Asian Banking & Finance (ABF), a Singapore-based publication, recognizing its initiatives in customer experience and service innovation.

Companies - Tue, July 7, 2026 | 12:42 pm GMT+7