Vietnam government has plan to boost economic growth

VinaCapital’s chief economist Michael Kokalari highlights a series of measures taken by the Vietnamese government to stir growth amid global economic headwinds.

Vietnam’s GDP growth slowed from 8% in 2022 to just 3.3% in Q1/2023, prompting the government to launch several initiatives to boost the country’s growth. These include tax cuts, monetary stimulus, and administrative measures aimed at easing the current difficult conditions in the real estate market, which we discussed in our previous reports and webinars.

The details of these and other initiatives are discussed below; the key points are that the government is proactively addressing the current growth slowdown and has ample fiscal resources to counter any continued growth headwinds (Vietnam’s government debt-to-GDP ratio was just 40% at the end of 2022).

We are confident that policymakers can counter the growth slowdown, and that Vietnam’s economic growth will rebound in the second half of 2023 for reasons discussed below – although it’s unlikely that the government can achieve its 6.5% GDP growth target this year.

Stock markets typically climb in advance of economic recoveries, so the government’s mounting resolve to support economic growth, coupled with the fact Vietnamese stocks are currently trading at a near 10-year low valuation, make now an auspicious time to invest in Vietnamese stocks, in our view.

The current slowdown in Vietnam’s economic growth is being caused by a drop in demand for “Made in Vietnam” products from U.S. consumers, although orders at FDI factories in Vietnam are likely to recover in H2/2023, which should help drive an economic rebound later this year.

Manufacturing contributes nearly one-quarter of Vietnam’s GDP and output contracted slightly in Q1/2023 versus 9% growth in 2022, because most products produced in Vietnam are exported to the U.S. and other developed countries. Note that Vietnam’s international trade accounts for a higher percentage of the country’s GDP than in any other economy in modern history (excluding economies like Hong Kong and Singapore), so weaker demand in the rest of the world weighs fairly heavily on Vietnam’s economy.

Specifically, Vietnam’s exports fell 12% year-on-year in Q1, driven by a 20% drop in exports to the U.S. Meanwhile, inventories at U.S. retailers and other consumer-facing firms such as Nike and Lululemon are now contracting, which is why we expect FDI factories’ order books to start recovering later this year (inventory growth at U.S. retailers peaked at over 20% yoy in late-2022, is currently around 10%, and looks likely to fall to 0% year-on-year growth in H2, which should prompt a resumption of order growth for FDI factories in Vietnam).

Finally, domestic consumption in Vietnam continues to grow at a healthy pace and consumer confidence has remained remarkably resilient despite the steep slowdown in GDP growth.

That is partly because the number of people who are employed grew by over 2% year-on-year in Q1, which more than twice the country’s population growth rate and we estimate that wages are up over 7% year-on-year, far outpacing CPI inflation which is just over 3%.

In addition, foreign tourist arrivals rocketed to over 60% of pre-Covid levels in Q1, despite the fact that Chinese tourists have not yet returned to the country en masse - which is another reason we expect Vietnam’s economic growth to recover in H2.

Measures to support growth

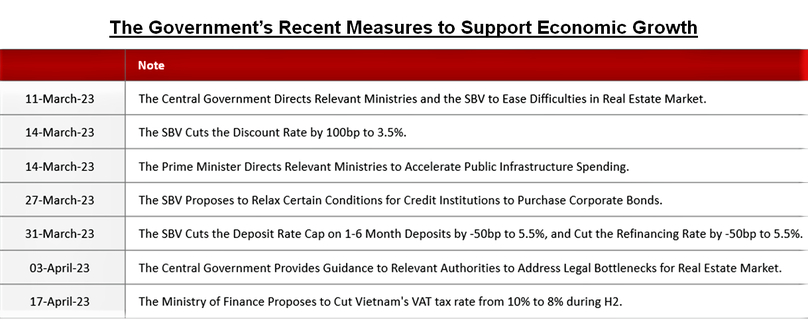

This week, Vietnam’s Ministry of Finance (MoF) finalized a plan to cut Vietnam’s VAT tax rate from 10% to 8% in H2/2023, which will equate to about $1.5 billion of stimulus for Vietnam’s $450 billion economy.

The government will also allow companies and individuals 3-6-month delays in the payment of various taxes. Last month, the State Bank of Vietnam (SBV) cut policy rates in Vietnam by 50-100 basis points, including a 50 basis-point reduction in the re-financing rate (which is the most important policy rate in Vietnam) to 5.5%, and a 50 basis-point reduction in the maximum interest rates banks are allowed to pay savers on deposits of up to 6 months to 5.5%.

In addition to those concrete steps to boost growth, the government also walked back some new regulations that were introduced in late 2022 to impose stricter conditions on the issuance of corporate bonds.

Vietnam’s government also directed its ministries to address various administrative bottlenecks that are impeding real estate development and infrastructure projects. The tax cuts and policy interest rate cut are the most concrete actions the government took to support growth, but these administrative measures could potentially have a much bigger impact on economic growth.

Real estate development, which accounts for nearly 10% of Vietnam’s GDP, has essentially ground to a halt, largely because of the difficulties developers are having obtaining the approvals required to proceed with their projects. Some of the micro-level issues that the government’s recent actions seek to address include bottlenecks entailed in converting agricultural land for use in residential real estate projects and delays in the appraisal of land values for the determination of land-use/conversion fees payable to the government.

The government also launched a $5.1 billion subsidized loan package to support the development of over one million new affordable housing units (subsidized loans will be provided to both developers and home buyers via the state-owned commercial banks) and established a new working group to review and remove obstacles developers encounter in progressing their development projects.

Further to that last point, the government also established a working group to accelerate the disbursement of public investment projects this year; it aims to increase infrastructure spending by about 40% in 2023 (to $30 billion), but infrastructure spending increased by less than 20% year-on-year in Q1.

Finally, in addition to the administrative measures above, the government also provided guidance intended to make it easier for banks to restructure loans extended to real estate developers, as well as to other borrowers, although the details of these proposed forbearance measures are still being hashed out.

Monetary policy easing

The interest rates that banks pay savers in Vietnam increased by over 200 basis points in 2022 to over 8% for 12-month deposits as of end-2022, although one-year deposit rates had climbed to above 9.5% at their peak in late-2022.

This surge in deposit rates is an additional source of difficulties for the real estate market, compounding the administrative issues mentioned above that are impeding real estate development projects. Mortgage rates in Vietnam are linked to long-term deposit rates, and higher deposit rates encourage savers to park their money in the bank rather than seek out other investments (such as real estate and/or investing in the stock market).

We believe that a 200bp drop in the average level of 12-month deposit rates from the levels at the beginning of this year (to circa 6%), would help drive a recovery in Vietnam’s real estate market and would support Vietnamese businesses in general. The SBV’s 50-100bp policy rate cut has put some downward pressure on long-term deposit rates – which have fallen by about 50bps year to date – but for deposit rates to fall significantly further, liquidity in Vietnam’s banking system will need to improve significantly.

Credit growth in Vietnam has outstripped deposit growth by about 3 percentage points annually over the last year, which has pushed up banks’ loan-to-deposit ratios to unacceptably high levels and prompted banks to increase the interest rates they pay savers in order to raise deposits. The government is addressing this liquidity shortage in a few ways, the most important of which is by purchasing the U.S. dollar from commercial banks to increase its forex reserves.

We expect the SBV to purchase about $25 billion of forex reserves this year, which would inject significant liquidity into the banking system and would likely boost Vietnam’s system-wide deposit growth by 4 percentage points this year, ceteris paribus, because the central bank typically purchases USD from the country’s commercial banks with newly printed Vietnam dong.

In short, the SBV’s purchases of forex reserves, coupled with the other measures the government is taking to ease liquidity in the banking sector are even more important monetary easing measures than the SBV’s policy rate cuts last month.

Finally, we mentioned above that the SBV cut the maximum allowable interest rate on 6-month deposits by 50 basis points last month. The interest rates on short-term deposits in Vietnam had already peaked in late-2022, and the March policy rate cut will put additional downward pressure on those deposit interest rates.

Consequently, there will be many bank deposits maturing in Q2 and Q3 and savers will essentially face a choice of rolling over their deposits at lower interest rates or plowing that money into the stock market (the vast majority of time deposits in Vietnam are 3-month and 6-month deposits).

Conclusions

GDP growth in Vietnam slowed precipitously in Q1 as consumers in the U.S. and other developed markets bought fewer “Made in Vietnam” products. This was exacerbated by the ongoing slowdown in the country’s real estate market, although a rebound in foreign tourist arrivals is mitigating the negative impact of these two burdens on Vietnam’s growth this year.

The government has taken a series of initiatives to address the country’s slowing growth, the most concrete of which are tax cuts and interest rate cuts, but administrative measures that are intended to ease bottlenecks impeding real estate development and infrastructure projects could have an even bigger impact to support growth in 2023 and beyond.

The government’s initiative to address disappointing Q1 GDP growth, coupled with the fact that FDI factories’ orders are likely to accelerate in H2, leads us to expect a rebound in GDP growth in the second half of this year. The fact that stock markets tend to start climbing in advance of economic rebounds, coupled with the fact that the VN-Index is trading at around a 10-year low valuation, leads us to believe that now could be an ideal time for investors to selectively purchase Vietnamese stocks.

We are encouraged to see that foreign investors have been net buyers year to date, so there are already some investors that are recognizing the attractiveness of the current entry point for Vietnamese stocks.

- Related News

- Read More

Intel to continue expanding investment in Vietnam: exec

U.S. chipmaker Intel will continue expanding investment, supporting workforce training, and helping develop Vietnam’s semiconductor ecosystem as the country refines investment support mechanisms to retain large-scale high-tech projects, said its executives.

Industries - Fri, May 8, 2026 | 7:48 pm GMT+7

Vingroup’s VinMetal partners with Primetals for green steel complex in central Vietnam

Vingroup’s subsidiary VinMetal has signed a strategic cooperation agreement with global steel giant Primetals Technologies to develop a large-scale integrated steel complex in central Vietnam.

Industries - Fri, May 8, 2026 | 4:25 pm GMT+7

Hanoi pushes Sumitomo, BRG to accelerate $4.2 bln smart city project

Hanoi authorities have asked Japan’s Sumitomo and local conglomerate BRG Group to quicken the progress of the North Hanoi Smart City project as soon as legal procedures are finalized.

Real Estate - Fri, May 8, 2026 | 3:31 pm GMT+7

Moody's Ratings upgrades MBBank's deposit ratings to Ba2 from Ba3, outlook stable

Moody’s Ratings (Moody’s) has announced an upgrade of the local currency and foreign currency long-term deposit and issuer ratings for Military Commercial Joint Stock Bank (MB, HoSE: MBB) from Ba3 to Ba2, aligning with Vietnam’s sovereign rating (Ba2 positive). The outlook remains "Stable."

Banking - Fri, May 8, 2026 | 3:00 pm GMT+7

Vietnam welcomes leading Indian groups to expand energy, infrastructure cooperation: top leader

Vietnam is ready to create favorable conditions for capable Indian corporations and businesses to expand investment and operations in the country in line with its laws, while ensuring transparency and balanced interests among stakeholders, said Vietnam’s Party chief and President To Lam.

Economy - Fri, May 8, 2026 | 1:59 pm GMT+7

Vietnam airport operator ACV records slows disbursement for Long Thanh mega-airport project

Airports Corporation of Vietnam's (ACV) slow disbursement for the Long Thanh International Airport project, located in the southern province of Dong Nai, highlights implementation bottlenecks despite the company's strong profitability in Q1/2026 and substantial cash reserves for the country's largest aviation infrastructure project.

Companies - Fri, May 8, 2026 | 1:41 pm GMT+7

Vietnam property developers shift to asset-holding strategy for stable cash flow

Vietnamese property developers are increasingly shifting away from the traditional build-to-sell model and focusing instead on accumulating long-term assets capable of generating stable recurring income, as the industry adapts to lessons learned from the market downturn of 2022-2023.

Real Estate - Fri, May 8, 2026 | 12:07 pm GMT+7

Vietnamese, Indian firms exchange 27 agreements on aviation, tourism, logistics, technology

Vietnamese and Indian firms on Thursday exchanged 27 cooperation agreements aimed at boosting trade, investment, tourism and training between the two countries, thereby making bilateral partnership deeper, more practical and effective.

Economy - Fri, May 8, 2026 | 11:13 am GMT+7

MBBank ranks among Vietnam's leading lenders for SME working capital in key industries

Military Bank (MB) has emerged as one of Vietnam’s leading providers of working capital financing for small and medium-sized enterprises (SMEs) operating in key economic sectors, according to National Credit Information Center (CIC) data.

Banking - Fri, May 8, 2026 | 8:56 am GMT+7

Hanoi eyes massive replanning of Red River corridor, relocation of riverside communities

Hanoi plans to gradually relocate and reorganize all residential areas outside the Red River dike system as part of an ambitious urban redevelopment strategy aimed at transforming both banks of the river into a new economic and cultural corridor for the capital.

Economy - Thu, May 7, 2026 | 5:04 pm GMT+7

Thaco, VinFast, TC Group urge Vietnam gov't to keep auto sector under conditional business rules

Vietnam’s three major domestic automotive corporations - Thaco, VinFast and TC Group - have urged the government to maintain automobile manufacturing, assembly and import activities within the list of “conditional business sectors,” warning that deregulation could weaken the country’s long-term industrial strategy and expose local producers to unfair competition.

Economy - Thu, May 7, 2026 | 4:09 pm GMT+7

Prudential Vietnam remits $194 mln in retained earnings to parent company

Prudential Vietnam transferred over VND5.1 trillion ($194 million) in retained earnings to its parent company, Prudential Corporation Holdings, earlier this year, according to disclosures in its 2025 financial statements.

Finance - Thu, May 7, 2026 | 3:33 pm GMT+7

$120 mln export ambition: What drives Vietnam’s home appliance giant Sunhouse to strengthen position in global supply chain?

The prominent presence of Sunhouse, Vietnam’s leading home appliance brand, at the 139th Canton Fair reinforces its strategic direction to become a key manufacturing partner in the global supply chain.

Companies - Thu, May 7, 2026 | 2:10 pm GMT+7

Vietnam makes 'huge difference' in terms of accessibility criteria: FTSE Russell exec

Vietnam has made “significant progress in meeting the requirements” over the past two years for an upgrade from frontier market to secondary emerging market status, said Wanming Du, FTSE Russell's Asia-Pacific director of index policy.

Finance - Thu, May 7, 2026 | 11:54 am GMT+7

Taiwan's electronics major Lite-On to pump additional $149 mln into Vietnam arms

Taiwanese electronics maker Lite-On Technology plans to inject an additional $149 million into its wholly owned subsidiaries in Vietnam, as part of efforts to expand production capacity and strengthen its manufacturing footprint.

Industries - Thu, May 7, 2026 | 8:00 am GMT+7

FedEx forms strategic tie-up with Viettel Post in push for Vietnam expansion

FedEx Express and Viettel Post, an arm of Vietnam's military-run telecom giant Viettel, have announced a strategic partnership with a view to strengthening nationwide delivery capabilities and enhance cross-border logistics connectivity.

Companies - Wed, May 6, 2026 | 5:16 pm GMT+7

- Travel

-

Work on $92 mln eco-urban resort project starts in northern Vietnam tourist hotspot

-

Royal Shore Beachclub announces grand opening in Hoi An

-

Sun Group partners with Keppel to drive green transition across tourist places

-

Sun Group starts work on Phan Thiet airport project in central Vietnam

-

ACV proposes shifting most international flights from Tan Son Nhat to Long Thanh by 2027

-

Sun Group, Dragone partner to elevate Vietnam’s live entertainment scene