China’s re-opening will only modestly boost Vietnam’s 2023 GDP growth

VinaCapital’s chief economist Michael Kokalari explains why the Vietnamese economy would not see a major impact from China’s 2023 re-opening.

China is Vietnam’s biggest trading partner, and investors, policymakers, and others have asked about the impact that China dropping its “Zero Covid” restrictions will have on Vietnam. There was some initial uncertainty, and even skepticism, about how quickly China would remove its Covid restrictions after the December 7 announcements from key government officials.

Last week, China dropped many Covid testing requirements, scrapped contact tracing, and essentially stopped reporting Covid case numbers. Meanwhile, China’s Central Economic Work Conference (CEWC) reiterated the government’s commitment to an “overall improvement” of, and “reasonable growth” for China’s economy next year.

Given all of the above, a consensus is now forming that China’s domestic consumption growth will surge from about 0% in 2022 to about 7% year-on-year in 2023, and that China’s energy usage will grow by about 10% next year.

Consequently, investors and others are enquiring about how Vietnam might benefit from a resumption of Chinese consumption growth, although concerns are also mounting about the possibility that China’s reopening will exacerbate inflation, both in Vietnam and globally.

We expect China’s re-opening to boost Vietnam’s GDP growth by over 2 percentage points next year, driven by the full resumption of Chinese tourist arrivals in the second half of 2023 (note that Vietnam Airlines resumed some flights to China on December 9 and that Chinese visitors accounted for one-third of Vietnam’s total tourist arrivals, pre-Covid).

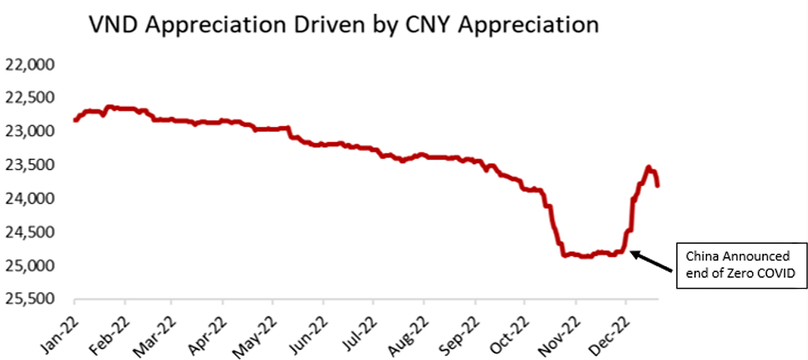

We also anticipate modest inflation pressures from China’s re-opening next year and note that inflation pressures in the rest of the world have clearly peaked and are now abating. Finally, while the most important impact of China’s re-opening on Vietnam is a likely full resumption of Chinese tourist arrivals in the second half of 2023, the most immediate impact has been an improvement in the sentiment towards the Vietnamese dong.

The value of the dong appreciated by over 5% during the last week in November and the first week in December (which was the time frame that encompassed China’s December 7 zero-Covid policy shift), driven by a circa 5% appreciation in the value of China’s currency over those two weeks.

The dong had depreciated by as much as 9% in mid-November due to this year’s surge in the value of the US dollar, so the dollar’s recent, modest decline also helped ease depreciation pressure on the dong, but the surge in the value of China’s currency was the primary factor the drove the rebound in the value of the dong that can be seen in the chart above.

Further to that last point, the value of the US dollar/DXY Index was essentially unchanged during the above-mentioned two weeks, and some fairly negative news about Vietnam’s trade balance and balance of payments came out during those two weeks, both of which make it clear that it was the appreciation in the value of the renminbi (CNY) that drove the appreciation of the dong.

It’s not obvious from an economic point-of-view why the recent appreciation in the CNY prompted an appreciation in the dong; Vietnam has a consistent 17%/GDP trade deficit with China, and an appreciation in China’s currency versus the dong exacerbates Vietnam’s trade deficit with China in the short-term via the so-called “J-Curve Effect”.

That said, market sentiment often overwhelms economic factors in FX markets, and the positive sentiment that China’s re-opening spawned led to a sharp appreciation in both the value of the CNY and the value of the dong. The opposite occurred in August 2015, when the sudden 3% depreciation in the value of China’s currency triggered an immediate 3% depreciation in the value of the dong, despite Vietnam benefitting from China’s depreciation.

We expected a similar sentiment phenomenon to boost the VN-Index, but we observe that China’s stock market achieved only a modest bounce in response to the government lifting its Covid restrictions and that Vietnamese investors are currently, primarily focused on various domestic issues that have impacted the market this year.

Impact on GDP growth

China is Vietnam’s largest trading partner, but Vietnam’s exposure to China’s domestic economy is quite modest, resulting in Vietnam’s GDP growth not being significantly hindered by Chinese Covid restrictions that impacted as much as one-quarter of that country’s economy this year.

Vietnam’s export growth to China was nearly flat in the first nine months of 2022, but only 14% of Vietnam’s exports are sold to China, so Vietnam’s GDP soared 8.8% year-on-year despite China’s lockdowns, in part because exports to the U.S. and the EU, which account for nearly one-half of Vietnam’s total exports, grew by 25% year-on-year in the first nine months of the year.

Furthermore, most of Vietnam’s exports to and imports from China are of production inputs and/or other intermediate goods entailed in the manufacture of electronics and garments accounting for two-thirds of the trade between the two countries. Some Vietnamese companies will benefit from China’s reopening, such as those that sell seafood and other agricultural products, but exports of products that are ultimately consumed by Chinese customers only account for around 5% of Vietnam’s total exports.

Effect on tourism, FDI

Foreign tourism contributed about 10% of Vietnam’s GDP pre-Covid, and foreign tourist arrivals are on track to reach 25% of pre-Covid levels this year.

We expect the number of foreign tourists will climb above 50% of pre-Covid levels in 2023 based on the assumption that Chinese tourist arrivals fully recover in the second half of next year. However, the pace of recent developments in China points to a possible faster full resumption of Chinese tourist arrivals, which could lead to an even larger contribution to Vietnam’s GDP growth next year than we currently expect.

We are aware of the concerns some investors have that the re-opening of China’s economy could detract from Vietnam’s appeal as a destination for FDI investment.

We see no possibility of this happening given that China has irrevocably damaged its appeal as an investment destination for multinational firms, and U.S.-China trade tensions have dramatically escalated this year.

Concerns about China’s increasingly erratic policy pronouncements are well publicized but we would emphasize that Chinese authorities held steadfast to the country’s “zero-Covid” policy for years and then abruptly dropped the policy, following what amounted to a one-day warning, when the Politburo announced its desire to “push for an overall improvement in the economy.”

U.S.-China trade tensions prompted multinational manufacturers to re-locate production facilities from China to Vietnam, or to set up new factories in Vietnam instead of China, evidenced by the fact that Vietnam’s trade surplus with the US tripled (from $25 billion in the first nine months of 2018 to $75 billion in the first nine months of 2022) while its trade deficit with China widened (from $19 billion to $52 billion over that same time period).

The Biden administration dramatically escalated trade tensions with China this year by announcing what amounts to an indefinite extension of Trump’s tariffs on imports from China, and with other severe measures, including a prohibition for US persons to work at some chip factories located in China.

Readers should also recall that there were already strong structural factors prompting FDI inflows to Vietnam before U.S.-China trade tensions emerged. Factory wages in Vietnam are around two-thirds below those in China, but the quality of Vietnam’s workforce is comparable to that of China according to surveys by the Japan External Trade Organization and others. Also, Japan and South Korea, which account for over half of Vietnam’s FDI inflows, both face serious demographic and intractable economic issues that compel companies in both countries to invest abroad.

China’s re-opening is expected to put upward pressure on food prices in Vietnam. Photo courtesy of Industry & Trade newspaper.

Impact on inflation

Many economists believe China’s re-opening could fuel global inflation, but there is no concrete consensus that China’s re-opening will do so.

Some analysts argue that a resumption of Chinese production could help further ease the supply chain tensions that account for about half of the current US inflation rate, according to economists at the US Federal Reserve.

We expect China’s re-opening to put upward pressure on food and energy prices in Vietnam (which account for nearly half of the CPI basket) and note that some well-placed Chinese economists expect a 20% increase in Chinese pork prices next year, for example.

In the past, surges in Chinese food prices understandably drove Vietnamese food prices higher given the geographic proximity of the two countries, but there are some factors that are likely to limit the surge in China’s inflation rate (including food price inflation) in the first half of 2023.

First, China’s mandatory government lockdowns appear to be giving way to voluntary lockdowns in the country’s cities (which account for about 80% of the country’s consumption) because of widespread concerns among the population about contracting Covid at a time when the country’s hospitals are likely to be overwhelmed.

Consequently, economic activity and price pressures in China are both likely to get worse before bottoming out sometime in Q1. Epidemiologists at the University of Hong Kong expect China’s Covid wave to peak around late January.

Finally, China’s reopening boom will not be as powerful as the reopening in the U.S. and Europe because unlike the governments in much of the developed world, China did not over-stimulate its economy with freshly printed money and direct stimulus payments to individuals. Consequently, China’s money supply growth, which fuels consumer price inflation, remained modest through Covid, and there is less “pent up savings” in China to drive a surge in the country’s consumption and consumer prices.

Conclusion

Analysts and economists generally believe that China dropping its Covid restrictions will have a major impact on the economies of countries in Asia and around the world next year. We expect China's reopening will have a bigger impact on the economies of other ASEAN countries than it will on Vietnam due to those countries’ greater exposure to China’s domestic economy.

The most immediate impact of China’s scrapping of its Covid restrictions has been a circa 5% appreciation in the value of the dong, driven by a 5% appreciation in the value of China’s currency.

That said, the major benefit that Vietnam will accrue from China’s re-opening is likely to be a circa 2 percentage point boost to GDP growth next year driven by a resumption of Chinese tourist arrivals.

Finally, China’s re-opening is likely to cause some upward inflationary pressure in Vietnam, the impact could be mitigated by several factors, including a more prolonged reopening compared to the U.S. and Europe, as well as less pent-up savings and demand in China compared to the U.S. and EU.

- Related News

- Read More

Vietnam Rubber Group plans capital hikes for listed subsidiaries as earnings climb

Vietnam Rubber Group (HoSE: GVR) plans to raise capital at several of its listed subsidiaries, starting with Phuoc Hoa Rubber, as the state-controlled giant seeks to strengthen its subsidiaries while benefiting from high rubber prices and expanding industrial park operations.

Companies - Wed, June 17, 2026 | 8:14 pm GMT+7

Vinhomes to cease land bank expansion in Vietnam, focus on capitalizing on existing projects

Vietnam’s largest listed property developer Vinhomes, a subsidiary of Vingroup (HoSE: VIC), will stop acquiring new land in the domestic market, shifting its focus toward developing its existing portfolio and extracting greater value from projects already under its control, chairman Pham Thieu Hoa said.

Companies - Wed, June 17, 2026 | 5:19 pm GMT+7

State-controlled machinery firm VEAM announces highest dividend payout in 4 years, stock listing still on hold

Vietnam Engine and Agricultural Machinery Corporation (VEAM) plans to pay more than VND6.96 trillion ($264.46 million) in dividends for 2025 at a payout ratio of 52.4%, its record high in four years, while its long-delayed stock exchange listing remains on hold due to unresolved legacy issues.

Companies - Wed, June 17, 2026 | 3:30 pm GMT+7

Aeon Mall Vietnam achieves double-digit growth in 2025, accelerates network expansion

Japan’s retail giant Aeon Mall continued to record strong growth in Vietnam last year while accelerating the expansion of its network in Danang, Thanh Hoa, Quang Ninh, and several other localities across the country.

Economy - Wed, June 17, 2026 | 2:53 pm GMT+7

Palm City project enters new development phase as Palm River subdivision launched

Nam Rach Chiec Company Limited, together with Huong Viet Properties, recently held the Palm City Urban Area kick-off ceremony and officially launched the Palm River subdivision, marking the beginning of a new development phase for the 30.2-hectare urban township in Ho Chi Minh City.

Real Estate - Wed, June 17, 2026 | 11:27 am GMT+7

Petrovietnam's assets top $44.8 bln in 2025, profit jumps 39%

Petrovietnam ended 2025 with total assets exceeding VND1,178 trillion ($44.8 billion), up nearly VND100 trillion ($3.8 billion) from a year earlier, while reporting a 39% increase in net profit and maintaining one of the country's largest cash positions.

Companies - Wed, June 17, 2026 | 8:00 am GMT+7

Coteccons dismisses concerns over executive departure, competition from Vingroup's arm

Vietnam's leading contractor Coteccons (HoSE: CTD) said a recent change in senior management was unrelated to the company's share price performance, as executives highlighted record order backlog and accelerating earnings growth amid a recovery in Vietnam's construction industry.

Companies - Tue, June 16, 2026 | 5:26 pm GMT+7

VinaCapital lists 2 strategic ETFs as Vietnam fund market broadens

Vietnam’s leading investment management firm VinaCapital has listed two strategic exchange-traded funds (ETFs) on the Ho Chi Minh City Stock Exchange, expanding investment options for investors seeking targeted exposure to Vietnam's long-term economic growth themes.

Finance - Tue, June 16, 2026 | 4:39 pm GMT+7

Oil & gas industry gives Vietnam edge in offshore wind supply chain: Global Wind Energy Council CEO

Vietnam is well positioned to play a significant role in the offshore wind power supply chain thanks to its established manufacturing base and expertise developed through its oil & gas industry and existing wind power projects, according to Ben Backwell, CEO of the Global Wind Energy Council (GWEC).

Energy - Tue, June 16, 2026 | 4:31 pm GMT+7

Vietnam banking, retail, oil stocks well placed for market recovery: brokerages

Vietnamese banking, retail and oil-gas stocks are among the sectors best positioned to benefit from a potential market recovery after months of pressure from geopolitical tensions and macroeconomic headwinds, according to local brokerages.

Finance - Tue, June 16, 2026 | 1:04 pm GMT+7

Petrovietnam, Huawei discuss cooperation in digital transformation, AI, energy technologies

State-owned Petrovietnam and China's Huawei Technologies discussed potential cooperation in digital transformation, artificial intelligence and digital energy infrastructure during a meeting last week, as the Vietnamese giant seeks to modernize its operations and expand into new energy sectors.

Companies - Tue, June 16, 2026 | 12:20 pm GMT+7

Over 38% of Vietnamese businesses still face informal costs despite reforms: survey

More than 38% of businesses in Vietnam still pay informal charges, highlighting persistent gaps between regulatory reforms and their implementation, according to a survey by the Vietnam Chamber of Commerce and Industry (VCCI).

Economy - Tue, June 16, 2026 | 11:26 am GMT+7

China ready to expand railway, power connectivity with Vietnam: PM

China is prepared to strengthen railway cooperation and enhance power grid connectivity with Vietnam, thereby expanding logistics corridors, trade links, and energy cooperation, said Chinese Premier Li Qiang during a phone talk with his Vietnamese counterpart Le Minh Hung on Monday.

Economy - Tue, June 16, 2026 | 8:52 am GMT+7

VN-Index approaches 1,800-point mark as easing Middle East tensions lift sentiment

Vietnam's benchmark VN-Index edged closer to the 1,800-point threshold on Monday as improving sentiment over easing tensions in the Middle East boosted risk appetite, driving gains in brokerage stocks while oil and Vingroup-related stocks weighed on the market.

Finance - Mon, June 15, 2026 | 8:34 pm GMT+7

Japanese products dominate Vietnamese consumer trust, but younger shoppers rewriting rules

Japanese products continue to enjoy the highest level of trust among Vietnamese consumers, reinforcing the country’s position as the benchmark for quality and reliability in one of Southeast Asia’s fastest-growing consumer markets, according to a new survey by market research firm Q&Me.

Economy - Mon, June 15, 2026 | 6:48 pm GMT+7

VinEnergo ramps up renewable energy push with 4 new subsidiaries

VinEnergo, the energy arm of Vietnamese conglomerate Vingroup, has accelerated its expansion into the power sector, establishing four new subsidiaries within a week as it builds a growing portfolio of renewable energy and infrastructure projects across Vietnam.

Companies - Mon, June 15, 2026 | 4:52 pm GMT+7

- Travel

-

Sun PhuQuoc Airways launches Singapore route, connecting two of Asia's 'paradise' islands

-

Seta - A “silken thread” weaving contemporary Cantonese cuisine into the soul of Phu Quoc

-

Danang airport starts $57 mln terminal expansion

-

Asia’s leading luxury travel magazine hails Hanoi's new opera house: 'Move aside, Sydney'

-

Work on $92 mln eco-urban resort project starts in northern Vietnam tourist hotspot

-

Royal Shore Beachclub announces grand opening in Hoi An